Why Africa is Back in the Focus of the mVAS Industry

Last week, several news stories from emerging markets caught the attention of the mVAS community. A payment platform for farmers was launched in Malawi, Vodacom M-Pesa Tanzania announced an alliance with PayPal, and PayPoint Group acquired Aperidata to embed open banking into its payment stack. At first glance, these seem like disparate fintech events. But for operators, aggregators, and advertisers working with direct carrier billing (DCB) and mobile subscriptions, these are signals of the same system: the mobile money infrastructure in developing countries is becoming mature enough to open fundamentally new monetization corridors.

Emerging markets are not just “large untapped audiences.” They are environments with unique structures of solvency, bank card penetration, and trust in telecom operators. And this is exactly where DCB has historically played the role of the primary payment rail for digital content. The emergence of new mobile payment platforms is changing the landscape: they create competition but simultaneously build out the infrastructure that increases the overall readiness of users to pay for digital services from their mobile phones.

What Happened: Three Cases of the Week

Payment Platform for Farmers in Malawi

A specialized payment platform for farmers has been launched in Malawi. This is not the first instance of mobile money in the country—Airtel Money and TNM Mpamba have been operating here since the 2010s. But the new platform targets a specific segment: smallholder agricultural producers who previously operated exclusively in cash. For the mVAS industry, this means the emergence of a new audience that, for the first time, has a digital wallet tied to a phone number.

M-Pesa and PayPal in Tanzania

Vodacom M-Pesa Tanzania announced an alliance with PayPal. This allows M-Pesa users to make international payments and receive money from abroad directly into their mobile wallet. For mVAS operators, this is an important precedent: the integration of mobile money with international payment systems lowers the barrier for cross-border subscriptions and micropayments.

PayPoint and Aperidata: Open Banking Arrives

PayPoint Group acquired Aperidata to integrate open banking services into its payment stack. Although this is a UK story, it reflects a global trend: alternative payment methods (APMs) are actively being integrated into unified payment gateways. And it is these gateways that are increasingly competing with DCB for transactions in the lower price segment—where carrier billing previously dominated.

How Mobile Money is Changing the DCB Ecosystem

The fundamental question for mVAS players: is mobile money a competitor or a catalyst for carrier billing? The answer depends on the market and the segment.

Where mobile money competes with DCB:

- Subscriptions in the $1–5/week range—here, mobile wallets offer more transparent fees and a better user experience.

- One-time payments for digital goods—a user might choose a wallet over DCB if they have a balance.

- Markets with high mobile money penetration (Kenya, Tanzania, Ghana)—here, DCB is losing share in micropayments.

Where mobile money catalyzes DCB:

- New audiences getting a digital wallet for the first time (like farmers in Malawi)—they get used to paying from their phones, which increases readiness for DCB subscriptions.

- Markets with low bank card penetration—mobile money creates a “payment culture” that then flows into DCB.

- Cross-border flows—the integration of M-Pesa with PayPal simplifies accepting payments from diasporas, which indirectly increases demand for local digital content.

African GEOs for mVAS: Where to Look Right Now

Not all African markets are equally promising for DCB monetization. Here is a brief assessment based on key parameters: mobile penetration, mobile money maturity, regulatory environment, and operator DCB readiness.

Tanzania

Mobile money penetration is among the highest in East Africa. M-Pesa dominates, but Airtel Money and Halotel are also active. Integration with PayPal opens up international flows. DCB flows through Vodacom and Airtel work, but conversion heavily depends on operator tariff policies. Average revenue per user (ARPU) is low, but volume compensates.

Malawi

One of the poorest markets in the world, but with growing mobile penetration (around 50%). Mobile money services like Airtel Money and TNM Mpamba operate stably. The new payment platform for farmers expands the addressable audience. DCB flows are still narrow, but competition for payment channels is lower than in Kenya or Nigeria.

Nigeria

The largest market by population. MTN Nigeria is a key partner for DCB. Mobile money is growing, but banking penetration is also increasing. High potential, but also high risks: regulatory restrictions, chargebacks, and pressure on fees.

Ghana

MTN Mobile Money holds a dominant position. The mobile money market is mature, and DCB flows work through MTN and Vodafone. Competition with mobile money for micropayments is high, but the volume of the subscription base compensates.

Conversion of DCB Flows in Markets with Mobile Money

The main practical question for aggregators and content providers: how does the presence of mobile money affect the conversion of DCB subscriptions?

In mature mobile money markets (Kenya, Tanzania, Ghana), users are accustomed to two-factor authentication when paying via a wallet. This creates a paradox: on the one hand, the user is ready to pay from their phone; on the other, they expect transaction confirmation, which can reduce impulsive DCB subscriptions.

In new markets (Malawi, Mozambique, some West African countries), the situation is reversed. The user is just getting used to mobile payments, and a one-click DCB flow (operator PIN) seems simpler and faster than a wallet transfer. Here, DCB subscription conversion can be higher than in mature markets.

Practical observations on conversion:

- In markets dominated by M-Pesa, the conversion of DCB subscriptions in the $1–3/week range drops by 15–25% compared to markets without mobile money.

- In new mobile money markets, DCB conversion in the first 3–6 months after the launch of a payment platform can grow by 10–20% due to the overall growth of payment culture.

- Churn after a DCB subscription is higher in markets with mobile money—the user cancels the subscription faster if they see an alternative.

Regulation and Compliance: What is Changing

African regulators are increasingly demanding transparency in DCB flows. Central banks in Kenya, Tanzania, Nigeria, and Ghana are introducing double opt-in rules for mobile subscriptions, limiting auto-renewals, and requiring clear price displays.

This creates two challenges for mVAS players:

- Technical: subscription flows must be adapted to the requirements of each regulator. Double opt-in reduces conversion by 20–40%, but without it, the operator can block the DCB short code.

- Legal: content providers must register services with the regulator in each country, which increases time-to-market by 2–4 months.

The integration of mobile money with international systems (like M-Pesa + PayPal) adds another layer of compliance: cross-border payments fall under AML requirements and transfer limits.

Strategy for Aggregators and Content Providers

What should mVAS players do to leverage the expansion of mobile money in Africa to their advantage?

1. Diversification of payment channels. Do not rely solely on DCB. In markets with mature mobile money (Tanzania, Kenya, Ghana), add mobile wallet payments as an alternative to DCB. This reduces dependence on operator tariff policies and provides a fallback channel if the DCB short code is blocked.

2. Localization of content and pricing. A single $2/week subscription does not work across all markets. In Malawi, the average revenue per user is 3–4 times lower than in South Africa. Adapt your pricing grid: micro-subscriptions for $0.25–0.50/day might convert better than weekly packages.

3. Partnerships with mobile money. Instead of competing with M-Pesa and Airtel Money, integrate them into your payment stack. Aggregators that offer content providers a single API for DCB and mobile money gain an advantage in tenders.

4. Monitoring regulatory changes. Track central bank decisions on DCB and mobile money. A change in double opt-in rules can alter conversion by 30% in a week. Subscribe to newsletters from regulators in key GEOs and maintain legal contacts in each country.

5. Working with new audiences. The payment platform for farmers in Malawi is an example of how a new audience gets a digital wallet for the first time. Content providers who are the first to offer relevant content (agri-info, weather, market prices) can capture the loyalty of this audience before big players arrive.

Risks and Anti-Fraud

The expansion of mobile money in developing countries inevitably attracts fraud. For the DCB ecosystem, this means three types of risks:

- Premium SMS fraud: scammers use stolen numbers to subscribe to premium services. In new markets with weak KYC, this is especially relevant.

- Subscription fraud: a user subscribes, consumes content, and then disputes the charge via the operator or mobile wallet. In markets with mobile money, chargeback mechanisms work faster than through DCB.

- SIM-swap fraud: attackers gain control over a number and use it for DCB transactions and mobile wallet transfers.

Aggregators must implement multi-factor verification for new subscriptions, monitor anomalous patterns (spikes in subscriptions from one device, short sessions with rapid unsubscriptions), and work with operators to block fraudulent numbers.

Choosing a GEO: Checklist for mVAS Teams

Checklist: Evaluating a New GEO for DCB Monetization in Africa

- Mobile penetration is above 40% and growing

- There is at least one operator with a working DCB short code and transparent tariff policy

- Mobile money is present but does not completely dominate (market share of 30–60%)

- The regulator allows single opt-in or double opt-in with reasonable conversion

- The average ARPU allows setting a subscription from $0.25/day

- There is a local partner or legal contact for service registration

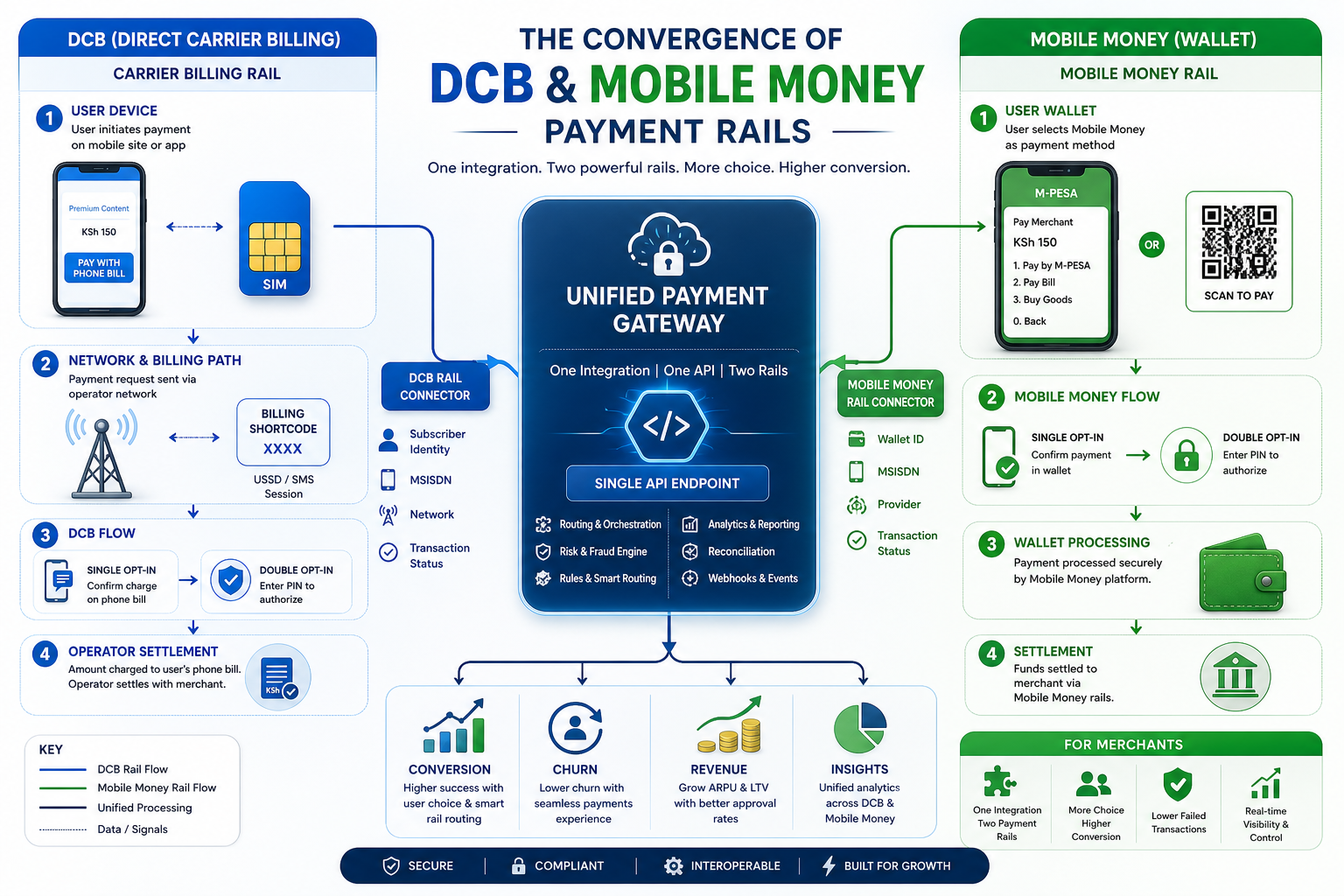

The Future: Convergence of DCB and Mobile Money

The integration of M-Pesa with PayPal is not an isolated event, but a trend indicator. Mobile money is ceasing to be an isolated national system and is becoming part of the global payment infrastructure. For the mVAS industry, this means that in 2–3 years, the boundary between DCB and mobile money may blur: operators will offer a unified payment API that automatically selects the optimal rail—carrier billing, mobile wallet, or open banking.

Aggregators who are already investing in multi-rail infrastructure will gain an advantage. Those who stick to pure DCB risk losing share in markets where mobile money offers a better user experience and lower fees for micropayments.

FAQ

Will mobile money kill DCB in Africa?

No, but it will change its role. DCB will remain the primary rail for impulsive subscriptions and micropayments in new and underdeveloped markets. In mature mobile money markets, DCB will lose share in the lower price segment, but will maintain its position in mid-range subscriptions and where mobile wallets are unavailable.

Which African GEOs are most promising for DCB right now?

Tanzania, Ghana, Nigeria, and Malawi. Each for its own reasons: Tanzania has mature mobile money and working DCB; Ghana has MTN MoMo dominance and a stable regulatory environment; Nigeria has audience volume; Malawi has low competition and a growing payment culture.

How does the M-Pesa and PayPal integration affect mVAS?

It simplifies the acceptance of international payments from diasporas and opens up the possibility of cross-border subscriptions. For content providers, this means a user in Tanzania can pay for content via M-Pesa topped up from abroad, which expands the addressable audience.

What to do if the regulator introduces double opt-in?

Adapt the subscription flow for two-step confirmation, test conversion on small volumes, optimize the SMS confirmation text, and consider alternative channels—mobile wallet or push notifications via the operator’s app.

Is it worth entering the Malawi market now?

Yes, if you are ready for low ARPU and a long ROI. The market is small, but competition is minimal, and the new payment platform for farmers creates a fresh audience. It is suitable for niche content providers rather than mass subscription services.