What Happened: Vodacom South Africa and Amazon Prime

In June 2026, Vodacom South Africa announced the launch of an Amazon Prime offer for its subscribers. At first glance, it reads like a routine story about yet another carrier-OTT partnership. But for the mVAS industry, it’s a signal of an ongoing shift: telecom operators are increasingly becoming not just billing channels, but full-fledged distributors of premium digital content, leveraging their subscriber base and Direct Carrier Billing (DCB) infrastructure.

The deal matters not in isolation, but as an illustration of a trend that directly affects aggregators, content providers, and advertisers working with mobile subscriptions. When a carrier of Vodacom’s caliber (part of the Vodafone Group with tens of millions of subscribers in South Africa) integrates a global streaming service, it reshapes the competitive landscape for everyone monetizing mobile content through DCB in the region.

Why Carriers Are Partnering with OTT Services

The logic behind carrier-OTT bundles is built on complementarity:

- The carrier gains a subscriber retention tool (reduced churn), a new revenue stream, and a way to monetize its subscriber base beyond traditional voice and data services.

- The OTT service (in this case, Amazon Prime) gains access to millions of users without bank cards, for whom paying from their phone balance is the only convenient way to subscribe.

- The subscriber gets a single bill, simplified onboarding, and often a discount or promotional period as part of their plan.

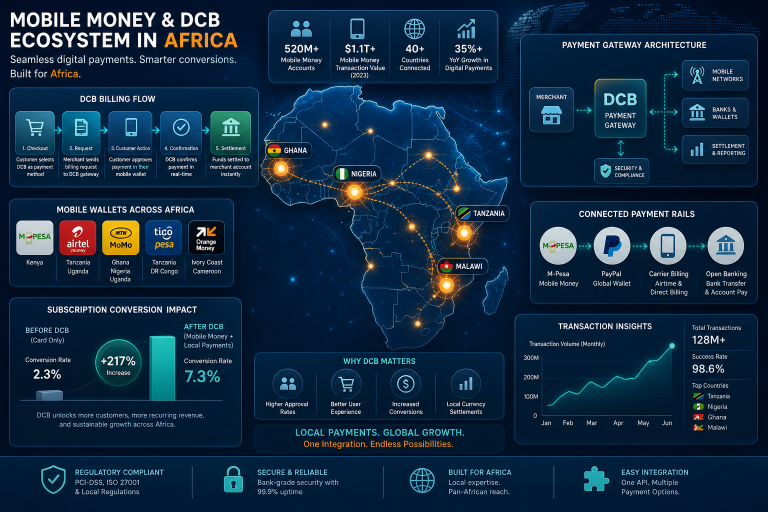

In regions with low bank card penetration (much of Africa, Southeast Asia, and Latin America), DCB remains a key payment rail. According to GSMA, hundreds of millions of women in low- and middle-income countries remain unconnected to the mobile internet — but those who are connected are more likely to have a phone with a balance than a bank card.

How Carrier+OTT Bundles Are Changing the DCB Ecosystem

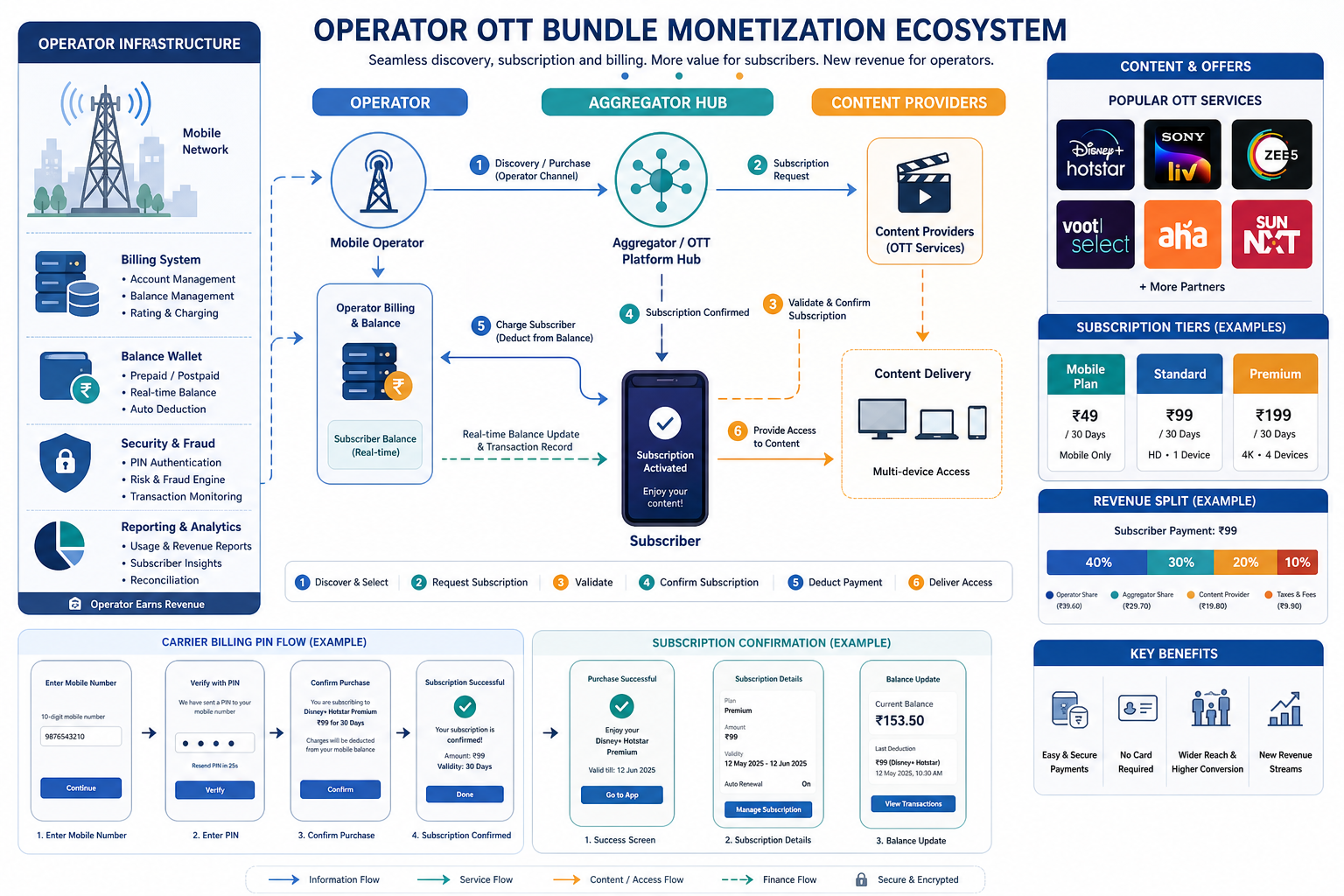

The traditional DCB monetization model in mVAS works like this: an aggregator connects to carrier billing platforms, a content provider supplies the product (a game, video, or content subscription), and traffic partners drive users through advertising. The subscription is charged to the phone balance, and revenue is split between the carrier, aggregator, and content provider.

The emergence of carrier bundles with global OTT services introduces a new element into this chain:

1. The Carrier as Content Distributor, Not Just a Billing Channel

Previously, the carrier provided the payment rail and took a commission. Now it sells Prime (or a similar service) subscriptions directly within its own app or via USSD/SMS channels. This means the carrier is competing with the very mVAS aggregators for subscriber attention to subscription content.

2. Rising Expectations for Content Quality

When a subscriber gets Amazon Prime through Vodacom, their benchmark for “mobile subscriptions” shifts. Local mVAS products — horoscopes, ringtones, simple games — start to look less attractive next to global streaming. This puts pressure on content providers: either raise the quality or find niches where global OTT players don’t operate.

3. Redistribution of Advertising Traffic

Affiliates and media buyers working with DCB offers in South Africa and neighboring countries find it harder to compete for clicks with branded Vodacom + Amazon promo campaigns. The carrier promotes the bundle through its own channels (SMS blasts, in-app push notifications, call centers), which reduces the share of organic traffic for third-party subscription products.

What This Means for DCB Aggregators

Aggregators that connect content providers to carriers find themselves in a dual situation. On one hand, carrier-OTT bundles validate the DCB subscription model itself — subscribers grow accustomed to paying from their balance for digital content. On the other hand, aggregators risk losing share if carriers start directly integrating global platforms.

Adaptation strategies for aggregators:

- Focus on niche and local content providers not covered by global OTT services: local sports, religious content, educational subscriptions, regional games.

- Develop proprietary technology infrastructure — antifraud, conversion analytics by carrier, A/B testing of PINs and subscription pages. Carriers find it easier to work with an aggregator that handles compliance and risk management.

- Expand into GEOs where carriers haven’t yet signed bundles with global streaming services. Africa is not a homogeneous market: in some countries, carriers actively bundle with OTT; in others, they don’t.

South Africa as a Case Study: Market Specifics

South Africa is one of the most developed telecom markets in Africa. Vodacom and MTN dominate, smartphone penetration is high, and DCB infrastructure is well-established. Launching Amazon Prime through Vodacom is a natural step for a market where subscribers are already accustomed to mobile subscriptions.

But for mVAS operators, this means intensifying competition in a high-conversion GEO. South Africa has traditionally been an attractive market for subscription DCB offers thanks to relatively high ARPU and good payment discipline. With global streaming entering through the carrier, a portion of the subscriber’s payment wallet is being reallocated.

Practical takeaways for operating in South Africa and similar markets:

- Monitor carrier bundles in real time — if Vodacom launches Prime, MTN will respond with an equivalent (Netflix, Disney+, or a local service).

- Adjust ad campaign targeting: subscribers already enrolled in a carrier bundle are less inclined toward additional subscriptions.

- Test cheaper micro-subscriptions (daily/weekly) that don’t directly compete with a monthly streaming subscription.

Impact on Conversion and Subscription LTV

One of the key questions for mVAS practitioners: how do carrier-OTT bundles affect conversion and lifetime value (LTV) of classic DCB subscriptions?

Data from markets where carrier-streaming bundles are already operating (Southeast Asia, select Latin American countries) shows mixed dynamics:

- In the short term, conversion for third-party subscription products can drop 5–15% at the moment a carrier bundle launches, especially if accompanied by aggressive promotion.

- In the medium term, the overall percentage of subscribers using DCB for subscriptions grows — the habit of paying from the balance for content strengthens.

- LTV of niche products (e.g., educational or gaming subscriptions) can even increase if they occupy a non-overlapping niche with streaming.

The key factor is wallet cannibalization. For a subscriber with a limited phone balance, every additional rand going to Prime is a rand that won’t go to another subscription product. But if the subscriber previously didn’t pay for digital content at all, the bundle can serve as an “entry ticket” into the world of mobile subscriptions.

Outlook for Content Providers

Content providers working through DCB should view carrier-OTT bundles not as a threat, but as an indicator of market maturity. A mature market with a subscription habit is a market where you can sell more complex and expensive products, provided they offer unique value.

Niches that remain resilient to competition with global streaming:

- Local content: regional series, sports, music in local languages. Amazon Prime doesn’t cover African local sports.

- Educational and kids’ subscriptions: demand is growing, but global OTT platforms poorly address these categories.

- Games and in-app purchases via DCB: mobile gaming through carrier billing remains a separate category where streaming bundles don’t create direct competition.

- Utility tools: VPNs, antivirus, cloud storage — products the subscriber buys not instead of streaming, but in addition to it.

Regulatory and Compliance Aspects

Carrier bundles with OTT services also raise compliance questions that affect the entire DCB ecosystem:

- Billing transparency: when a Prime subscription is included in a single carrier bill, the subscriber may not realize that part of their monthly payment is a subscription to a third-party service. Regulators in Africa (ICASA in South Africa) increasingly require separate display of such services.

- Unsubscription and refunds: if a subscriber cancels Prime through the carrier, how quickly does billing stop? Synchronization delays between the OTT platform and carrier billing create chargeback and complaint risks.

- Age restrictions: Amazon Prime includes 18+ content, and the carrier acting as distributor takes on responsibility for subscriber age verification.

For aggregators and content providers, this means that compliance standards set by the carrier in partnership with a global OTT partner will inevitably extend to other DCB products. If Vodacom implements two-factor verification for Prime, MTN and other carriers will soon require the same from all subscription products.

Global Context: Not Just Africa

The carrier-OTT bundle trend isn’t limited to South Africa or Africa. Similar deals are being struck worldwide:

- In India, Reliance Jio integrates streaming services into its tariff plans.

- In Southeast Asia, Telkomsel, Globe, and other carriers offer bundles with Netflix, Disney+, and local platforms.

- In Latin America, Claro and Movistar actively bundle with global OTT services.

For the mVAS ecosystem, this means the model of “carrier as billing rail” is evolving into “carrier as content aggregator and distributor.” DCB aggregators need to rethink their value proposition: not simply “we connect you to carrier billing,” but “we help you compete in an environment where the carrier itself sells content.”

Practical Steps for mVAS Teams

Checklist: How to Adapt Your DCB Strategy for the Era of Carrier-OTT Bundles

- Audit which of your GEOs already have or are planning carrier bundles with global OTT services — adjust conversion forecasts accordingly.

- Identify content niches that don’t overlap with streaming (local sports, education, games, utilities) and redistribute traffic.

- Test micro-subscriptions (daily/weekly) priced below streaming — they occupy a separate part of the subscriber’s wallet.

- Strengthen antifraud and compliance processes: standards set by the carrier for OTT partners will soon extend to all DCB products.

- Revisit payout models with content providers: if the carrier takes a higher commission on bundle subscriptions, revenue-share negotiations may shift.

- Monitor unsubscribe and chargeback rates: a single carrier bill may increase complaints about “unexplained charges.”

What Doesn’t Change

Despite all the transformations, the fundamental principles of DCB monetization remain unchanged. Phone balance as a payment rail is still indispensable in regions with low banking penetration. Conversion depends on the PIN, subscription page, onboarding speed, and offer relevance. Antifraud, compliance, and proper unsubscribe handling remain critical for long-term carrier relationships.

Carrier-OTT bundles aren’t killing DCB monetization — they’re transforming it. Those who can adapt will find new opportunities in a more mature, subscription-savvy environment.

FAQ

Do carrier-OTT bundles threaten classic DCB subscriptions?

There’s no direct threat, but there is a reallocation of the subscriber’s wallet. In the short term, conversion for third-party subscriptions may drop 5–15% at bundle launch. In the medium term, the overall volume of DCB payments grows as subscribers grow accustomed to paying from their balance for content.

Which content niches are resilient to competition from carrier-streaming bundles?

Local sports and content in local languages, educational and kids’ subscriptions, mobile games with in-app purchases via DCB, and utilities (VPN, antivirus, cloud storage). These categories don’t directly overlap with streaming services.

What should aggregators do if the carrier starts selling OTT subscriptions directly?

Focus on niche and local content providers, develop proprietary antifraud and analytics infrastructure, expand into GEOs where carriers haven’t yet signed OTT bundles, and offer carriers subscription product management services.

How do bundles affect compliance standards for DCB products?

When carriers integrate global OTT services, they implement heightened standards for billing transparency, age verification, and unsubscribe processes. These standards then extend to all DCB products operating through that carrier.

Should you exit the South African market because of Amazon Prime arriving through Vodacom?

No. South Africa remains a high-conversion GEO with well-established DCB infrastructure. You need to adapt your strategy: niche products, micro-subscriptions, and categories that don’t overlap with streaming. The market is maturing, not disappearing.