AI in Digital Payments: What’s Happening and Why the mVAS Industry Needs It

India’s UPI payment system processes over 750 million transactions a day and aims for the one billion mark. According to Dilip Asbe, CEO of National Payments Corporation of India, the next stage of growth is impossible without artificial intelligence—it’s needed for fraud prevention, credit distribution, and user acquisition. This isn’t an abstract forecast: NPCI is already working with the central bank and government on AI infrastructure.

For the mVAS industry—operators, aggregators, content providers, and advertisers—this experience is directly relevant. Direct carrier billing (DCB) and mobile subscriptions face the same issues: fraud, subscriber churn, low conversion at the payment confirmation stage, and regulatory pressure. The machine learning that NPCI is implementing for UPI can be adapted for DCB flows, anti-fraud scoring, and subscription funnel optimization.

In this article, we explore exactly how AI approaches from digital payments apply to DCB monetization, which models work for anti-fraud and conversion, and what aggregators and providers should do right now.

Why DCB is Vulnerable: The Risk Structure

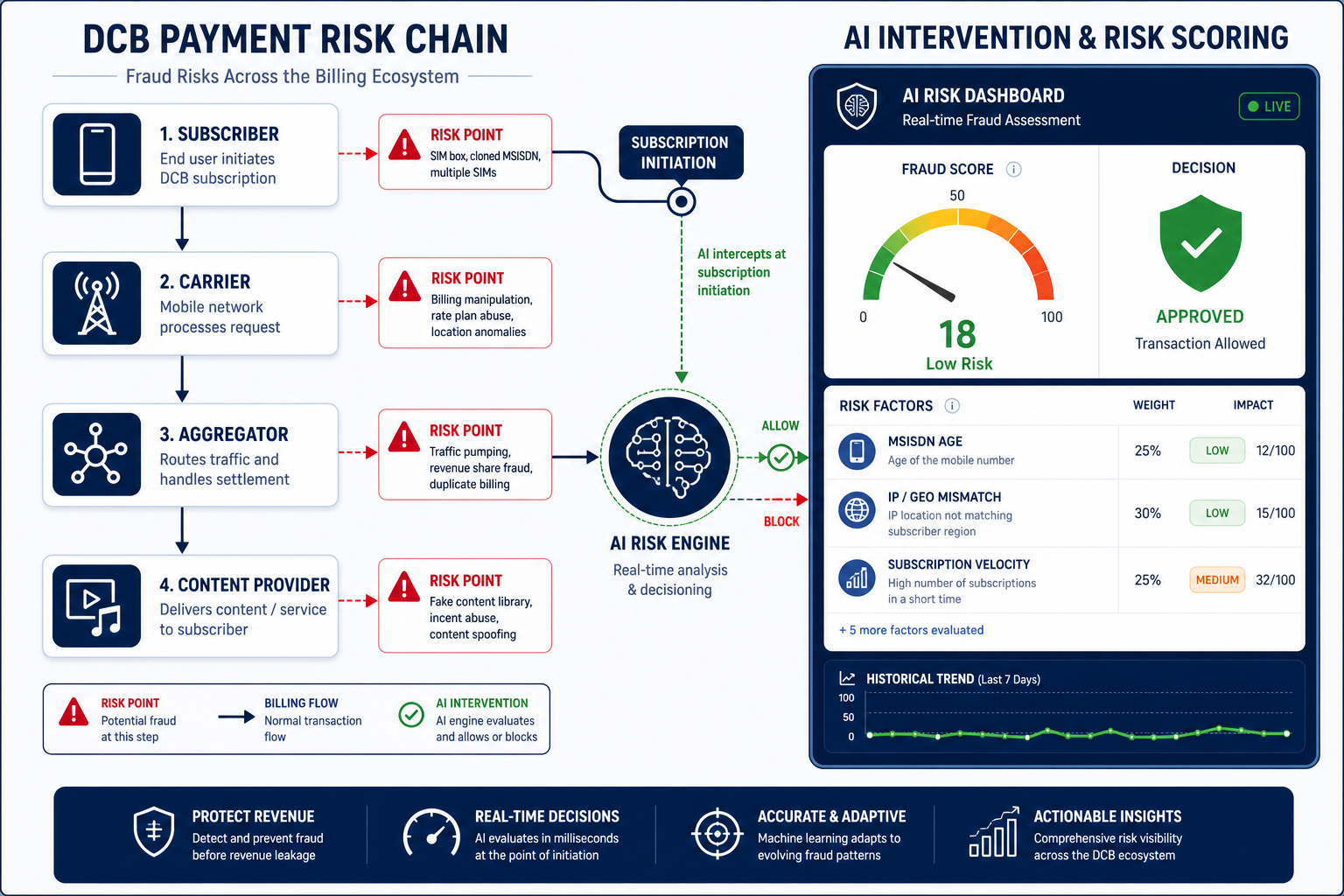

DCB payments go through a chain: user → mobile operator → aggregator → content provider. At each link, there are risk points:

- Premium SMS fraud — sending paid messages without the subscriber’s consent, a classic problem from the early 2000s that is returning in new GEOs.

- Subscription fraud — automatic billing after a “free trial period” that the user didn’t notice or understand.

- SIM-swap and account takeover — hijacking a subscriber’s number to deduct funds from their balance.

- Friendly fraud — a subscriber disputes a charge even though they subscribed themselves.

- Traffic fraud — an affiliate generates fake subscriptions through bot traffic or incentivized traffic.

Manual rules and static thresholds (limits on the number of subscriptions per hour, MSISDN blacklists) work but lag behind. AI allows moving from a reactive to a predictive model.

UPI Lessons: Three AI Directions Transferring to DCB

1. Real-Time Fraud Prevention

NPCI uses AI to analyze transaction patterns in real time: abnormal spikes, atypical geolocations, high-speed deduction sequences. For DCB, this means:

- Subscriber behavioral scoring — the model assesses the probability of fraud based on billing history, device type, time of day, GEO, and the operator’s tariff plan.

- Graph connections — identifying clusters of MSISDNs subscribing to the same content from a single IP range within a short window.

- Adaptive thresholds — instead of a fixed limit of “no more than 5 subscriptions per hour per MSISDN,” the model dynamically changes the threshold based on context.

2. Credit Scoring and Micro-loans on Balance

Asbe mentioned credit distribution via UPI as one of the AI directions. In the DCB ecosystem, this transforms into a predictive model of churn and default risk: which subscribers are 80% likely to cancel their subscription in the first 7 days, whose balance is near zero and the charge will fail, and who should be offered a cheaper tariff instead of losing them.

3. Onboarding the Next 500 Million Users

NPCI plans to use AI to onboard users from rural areas and groups with low digital literacy. For mVAS, this means personalizing subscription offers based on the subscriber’s profile: prepaid or postpaid, average ARPU, content consumption history, and language region.

How AI Changes Anti-Fraud in DCB: Specific Models

Subscription Scoring at Initiation

When a subscriber clicks “Subscribe,” the model evaluates in milliseconds:

- MSISDN age (new number = higher risk).

- Number of active subscriptions on the number.

- Ratio of successful to unsuccessful charges over the last 30 days.

- IP address match with the registered SIM region.

- Interaction pattern with the landing page (time on page, clicks, scroll).

The output is a score from 0 to 100. If the score is below 30, the subscription is blocked or sent for additional verification (SMS PIN code, USSD confirmation). If above 70 — it goes through without friction.

Affiliate Fraud Detection

Affiliate traffic is the main source of fraudulent subscriptions in mVAS. The AI model analyzes:

- Concentration of subscriptions from a single traffic source (publisher ID, sub ID).

- Ratio of subscriptions to unsubscriptions in the first 24 hours (high churn = fraud signal).

- Form filling patterns (bots fill in 0.3 seconds, humans in 3–7).

- MSISDN duplicates between different affiliates.

The model doesn’t just block but assigns a fraud score to each affiliate, allowing the aggregator to introduce differential payouts: clean traffic — full rate, gray — reduced, fraudulent — blocking and payout withholding.

Chargeback Pattern Monitoring

Chargebacks and complaints are the main signal to the regulator. The AI model tracks:

- An increase in complaints from a specific content provider.

- Geographic anomalies (a spike in complaints from one region).

- Correlation between a tariff change and an increase in unsubscriptions.

This allows the aggregator to react before the regulator or operator applies sanctions.

Conversion Optimization: AI for Subscription Funnels

Anti-fraud is half the battle. The second half is maximizing the conversion of legitimate traffic. Here, AI works at the intersection of data and UX.

Dynamic Tariff Selection

Instead of a single tariff for all subscribers, the model selects the optimal price based on:

- The subscriber’s ARPU over the last 3 months.

- Tariff plan type (prepaid/postpaid).

- Subscription history (whether there were subscriptions before, for what content).

- Region and local purchasing power parity.

For example, a subscriber with an ARPU of $2 per month is offered a subscription for $0.50/week, and one with an ARPU of $15 — for $3/week. This isn’t discrimination but adaptation to payment capacity, which increases overall conversion by 15–25% according to aggregators who implemented dynamic pricing.

Optimizing the Billing Moment

On prepaid plans, the moment of billing is critical. If the balance is near zero, the charge won’t go through, and the subscription will break. The AI model predicts the optimal window for billing based on the subscriber’s top-up pattern:

- When the subscriber usually tops up (in the morning on payday, in the evening after work).

- What the average balance is 3 days after top-up.

- The probability of a successful charge at any given hour.

The aggregator gets the opportunity to plan billing retries not randomly, but in the window with the highest probability of success.

Personalizing Content Offers

For content providers, AI opens up the possibility of A/B testing at the subscriber level:

- Subscribers who previously subscribed to video streaming are offered a video bundle.

- Subscribers with a history of gaming subscriptions are offered gaming content.

- New subscribers without history are offered a trial period with minimal friction.

Implementation Practice: What Aggregators and Providers Should Do

Implementing AI in DCB doesn’t require building your own neural network from scratch. Most tasks are solved based on ready-made ML platforms and APIs. Key steps:

Data Collection and Normalization

Without quality data, the model won’t work. The aggregator needs to collect:

- Logs of all subscription attempts (successful and unsuccessful) for at least 6 months.

- Complaint and chargeback data linked to MSISDN and content provider.

- Traffic attribution by sources (publisher, sub ID, campaign).

- Subscriber profile from the operator (where available under regulatory rules).

Model Selection and Training

For anti-fraud, gradient boosting (XGBoost, LightGBM) and graph neural networks for identifying clusters show the best results. For conversion optimization, these are recommendation systems based on collaborative filtering and predictive churn models.

Training is conducted on historical data labeled “fraud/not fraud” (based on chargebacks and manual reviews). The model is updated weekly.

Integration into the Payment Flow

The model must operate in real time with a delay of no more than 100–200 ms. This is achieved by:

- API call to the ML service at the moment of subscription initiation.

- Caching the score for repeated requests.

- Falling back to static rules if the model is unavailable.

Regulatory Risks and Compliance

AI in payments is not just technology, but a regulatory zone. Operators and regulators in the EU, India, and Latin America are increasingly demanding transparency in algorithmic decisions.

- GDPR and explainability: if the model blocks a subscription, the subscriber (and regulator) has the right to know why. A black box doesn’t pass compliance.

- Consent and double opt-in: AI doesn’t cancel the need for explicit consent to subscribe. It helps detect whether the consent was real or simulated.

- Data minimization: the model shouldn’t use more data than necessary. The subscriber profile is a minimal set of features.

Aggregators implementing AI anti-fraud are advised to document the model’s logic and have a manual review procedure for disputed cases.

What Not to Do: Common Mistakes

- Training the model on data from one GEO and applying it in another — fraud patterns in India and Latin America differ.

- Relying solely on AI — static rules remain the first line of defense. AI is the second.

- Ignoring the feedback loop — the model must be retrained on new data, otherwise fraudsters adapt faster.

- Blocking traffic by score without calibration — an uncalibrated model can cut off 20% of legitimate subscriptions.

Checklist: Implementing AI Anti-Fraud in DCB

- Collect subscription and complaint logs for 6+ months with fraud/not fraud labels

- Set up traffic attribution by publisher ID and sub ID to identify fraudulent sources

- Choose an ML model: XGBoost for scoring, graph networks for fraud clusters

- Integrate the model into the payment flow with a delay of up to 200 ms and a fallback to rules

- Set up weekly retraining on fresh data

- Document the model’s logic for regulatory compliance and dispute resolution

The Future: AI as a DCB Infrastructure Standard

The UPI experience shows that AI is ceasing to be a competitive advantage and becoming basic infrastructure. In mVAS, this means that in 2–3 years, operators will require AI anti-fraud from aggregators as a condition for connection. Regulators will require explainable models as a licensing condition. Affiliates will require dynamic pricing as a condition for work.

Aggregators and providers who start collecting data and training models now will have a 12–18 month window to build an advantage. Those who wait for ready-made solutions from operators will get someone else’s rules and thresholds.

FAQ

Do small aggregators need AI anti-fraud?

Yes, if the volume of subscriptions exceeds 50,000 per month. At lower volumes, static rules and manual review are sufficient. An AI model requires data for training, and on small samples, it overfits.

How much does it cost to implement AI in DCB anti-fraud?

Basic scoring on XGBoost with open libraries and cloud infrastructure costs $2,000–$5,000 per month for hosting and engineering. A full-fledged platform with graph models and real-time API — from $15,000 per month.

How does AI affect the conversion of legitimate traffic?

A properly configured model doesn’t reduce conversion but increases it by 5–15% by reducing false blocks and dynamic tariff selection. The main mistake is blocking by score without calibration, which cuts off legitimate subscribers.

Can AI be used to optimize billing retries?

Yes. The model predicts the optimal window for a retry based on the subscriber’s top-up pattern. This is especially effective on prepaid plans, where the billing moment determines success.

What to do if the regulator requires model explainability?

Use models with interpretable features (XGBoost with SHAP values) and document the top factors influencing the decision for each blocked subscription. Deep neural networks without an explainable layer are better not used for blocking.

Conclusions

The Indian UPI experience is not a theoretical model but a working infrastructure processing almost a billion transactions a day with AI anti-fraud and scoring. For the DCB industry, this means the technologies are already available and tested at scale. The question is not whether to implement AI, but who will do it first in their GEO and gain an advantage in conversion, fraud reduction, and subscriber retention.

mVAS aggregators and providers should start with data: collect, label, normalize. Without this, any model is an empty shell. With data, even basic XGBoost gives a tangible effect in the first month.